9

Best Low-Interest Personal Loans Of 2026: From 6.49% APR

Compare the Best Low-Interest Personal Loans of 2026

| COMPANY | FORBES ADVISOR RATING | APR RANGE | LOAN AMOUNTS | LEARN MORE |

|---|---|---|---|---|

|

7.24% to 24.89%

|

$5,000 to $100,000

|

via Credible.com's Website

| |

|

|

6.99% to 35.49%* with all discounts

|

$5,000 to $100,000

|

via Credible.com's Website

| |

|

6.74% to 26.49%

|

$3,000 to $100,000

|

via MoneyLion's Website

| |

|

|

8.74% to 24.99%

|

$1,000 to 50,000 for existing U.S. Bank customers and up to $25,000 for new customers

|

via MoneyLion's Website

| |

|

|

8.99% to 17.99%

|

$600 to $50,000

|

via MoneyLion's Website

|

The above personal loan rates and details are updated regularly. However, the annual percentage rates (APRs) and loan details may have changed since the page was last updated. Keep in mind, some lenders make specific rates and terms available only for certain loan purposes. Be sure to confirm available APR ranges and loan details, based on your desired loan purpose, with your lender before applying.

Best Low-Interest Personal Loans of 2026: A Closer Look

BEST OVERALL LOW-INTEREST PERSONAL LOAN

LightStream

APR range

7.24% to 24.89%

with autopay

Minimum Credit Score

700

7.24% to 24.89%

with autopay

700

LightStream offers loans with both a low minimum and maximum interest rate, along with a rate-beat program. LightStream’s unsecured personal loans range from $5,000 to $100,000 with loan amounts varying based on the loan purpose. In addition to offering appealing and flexible terms, LightStream charges no origination, late payment or prepayment fees. The lender also offers a 0.50% rate discount for borrowers who enroll in autopay.

- Does not charge origination, late payment or prepayment fees

- Lower maximum APR (capped at 24.89%)

- Same-day funding is possible

- Offers consolidation loan amounts of up to $100,000

- Higher minimum loan amount ($5,000)

- No option for prequalification

- No option for direct payments to creditors

- No mobile app

Lender Details

Eligibility

- Minimum credit score: 700

- Co-signers/co-borrowers: Co-borrowers accepted

Funding Speed

Same-day funding may be available if you sign documents, provide a bank account and complete the loan verification process before 2:30 p.m. ET.

BEST FOR LARGE LOAN LIMITS

SoFi®

APR range

6.99% to 35.49%*

with all discounts

Minimum Credit Score

Does not disclose

6.99% to 35.49%*

with all discounts

Does not disclose

SoFi is an online lending platform that offers unsecured fixed-rate personal loans in every state. Founded in 2011, SoFi has extended over $50 billion in loans and stands out for allowing high loan amounts and its availability of extended loan terms.

Loans are available from $5,000 to $100,000, making SoFi a great option for those with excellent credit who need to borrow a large amount of money. Loan amounts available may vary by the state you live in. Repayment terms range from two to seven years, making SoFi an incredibly flexible option for those with sufficient credit (minimum does not disclose) and annual income (at least $45,000). SoFi also lets prospective borrowers submit joint applications—although co-signers are not permitted.

Approved borrowers are rewarded with comparatively low APRs. What’s more, SoFi doesn’t charge origination fees, late fees or prepayment penalties—a stand-out feature because personal loan lenders often charge origination or late payment fees at a minimum. The platform also offers customers several other perks and discounts.

- Offers comprehensive member benefits and perks

- Does not charge origination, late payment or prepayment fees

- Offers direct payment to creditors

- Loan amounts of up to $100,000

- Higher minimum loan amount ($5,000)

- Longer average funding time (4 days)

- High maximum loan APR ( 35.49%*)

- Live chat is limited to business hours

Lender Details

Eligibility

- Minimum credit score: Does not disclose

- Co-signers/co-borrowers: Co-borrowers accepted

Funding Speed

Funds should generally be available within a few days after signing the loan agreement.

Disclosures

*Terms and conditions apply. SOFI RESERVES THE RIGHT TO MODIFY OR DISCONTINUE PRODUCTS AND BENEFITS AT ANY TIME WITHOUT NOTICE. To qualify, a borrower must be a U.S. citizen or other eligible status, be residing in the U.S., and meet SoFi’s underwriting requirements. Not all borrowers receive the lowest rate. Lowest rates reserved for the most creditworthy borrowers. If approved, your actual rate will be within the range of rates at the time of application and will depend on a variety of factors, including term of loan, evaluation of your creditworthiness, income, and other factors. If SoFi is unable to offer you a loan but matches you for a loan with a participating bank, then your rate may be outside the range of rates listed above. Rates and Terms are subject to change at any time without notice. SoFi Personal Loans can be used for any lawful personal, family, or household purposes and may not be used for post-secondary education expenses. Minimum loan amount is $5,000. The average of SoFi Personal Loans funded in 2024 was around $33K. Information current as of 06/03/26. SoFi Personal Loans originated by SoFi Bank, N.A. Member FDIC. NMLS #696891 (www.nmlsconsumeraccess.org). See SoFi.com/legal for state-specific license details. See SoFi.com/eligibility for details and state restrictions.

*Fixed rates from 6.99% APR to 35.49% APR. APR reflect the 0.25% autopay interest rate discount and a 0.25% SoFi Plus interest rate discount. SoFi Platform personal loans are made either by SoFi Bank, N.A. or , Cross River Bank, a New Jersey State Chartered Commercial Bank, operating from its Delaware branch, Member FDIC, Equal Housing Lender. SoFi may receive compensation if you take out a loan originated by Cross River Bank. These rate ranges are current as of 06/03/26 and are subject to change without notice. Not all rates and amounts available in all states. See SoFi Personal Loan eligibility details at https://www.sofi.com/eligibilitycriteria/#eligibility-personal. Not all applicants qualify for the lowest rate. Lowest rates reserved for the most creditworthy borrowers. Your actual rate will be within the range of rates listed above and will depend on a variety of factors, including evaluation of your credit worthiness, income, and other factors.

Loan amounts range from $5,000– $100,000. The APR is the cost of credit as a yearly rate and reflects both your interest rate and an origination fee of 9.99% of your loan amount for Cross River Bank originated loans which will be deducted from any loan proceeds you receive and for SoFi Bank originated loans have an origination fee of 0%-7%, will be deducted from any loan proceeds you receive.

Autopay: The SoFi 0.25% autopay interest rate reduction requires you to agree to make monthly principal and interest payments by an automatic monthly deduction from a savings or checking account. The benefit will discontinue and be lost for periods in which you do not pay by automatic deduction from a savings or checking account. Autopay is not required to receive a loan from SoFi.

Member Rate Discount: To be eligible for an additional 0.25% interest rate reduction on a Personal Loan, you must, within 31 days of loan funding, either (1) meet SoFi Plus eligibility criteria, (2) receive an Eligible Direct Deposit into a SoFi Checking or Savings account, or (3) receive at least $5,000 in Qualifying Deposits into a SoFi Checking or Savings account. You must continue to meet at least one of the above eligibility criteria every 31 days to maintain the discount. See the SoFi Plus terms for details on SoFi Plus subscription. For more details on Eligible Direct Deposit or Qualifying Deposits, please see https://www.sofi.com/legal/banking-rate-sheet.

Once you become eligible during the initial period, the discount will be removed or reinstated depending on whether the criteria have been met. Each time your loan is re-amortized, your monthly payment amount will change based upon the interest rate that was in place. SoFi reserves the right to modify or terminate this offer at any time for unenrolled participants. You are not required to meet these criteria to be approved for a loan.

BEST FOR SMALL LOANS

Wells Fargo

APR range

6.74% to 26.49%

with autopay discount

Minimum Credit Score

Does not disclose

6.74% to 26.49%

with autopay discount

Does not disclose

Wells Fargo offers fixed-rate personal loans with limits between $3,000 to $100,000 and repayment terms from 12 to 84 months. While longer term lengths, such as 84 months, will decrease your fixed monthly payment, you will pay more interest over the life of your loan compared to a loan with terms of, let’s say, 12 months.

Wells Fargo personal loans boast interest rates from 6.74% to 26.49% for customers who qualify for the 0.25% relationship discount. To qualify, you need to have a Wells Fargo checking account and make automatic payments from a Wells Fargo deposit account.

Although Wells Fargo is available to anyone in the United States, only current Wells Fargo customers will be able to apply online. New customers will need to visit a branch location. Wells Fargo does not have branch locations in Indiana, Kentucky, Louisiana, Ohio, Oklahoma, Maine, Massachusetts, Michigan, Missouri, New Hampshire, Vermont or West Virginia.

- Offers loan amounts of up to $100,000

- Low minimum APR (6.74%)

- Average 1-day funding timeline

- Requires borrowers to have a longstanding Wells Fargo checking account

- Charges a $25 monthly account fee (unless waived)

- No direct payment to creditors

Lender Details

Eligibility

- Minimum credit score: Does not disclose

- Co-signers/co-borrowers: Not accepted

Funding Speed

On average, borrowers get their loan funds within one business day.

BEST FOR EXISTING U.S. BANK CUSTOMERS

U.S. Bank

APR range

8.74% to 24.99%

with autopay

Minimum Credit Score

680

8.74% to 24.99%

with autopay

680

U.S. Bank is one of the largest banks in the country. In addition to banking, wealth management and business services, it also offers several lending products, including auto refinancing. Repayment terms range from 12 to 84 months.

Keep in mind that while you might get approved for refinancing through U.S. Bank with a credit score as low as 680, you’ll need a score of at least 800 to qualify for the lowest available interest rates. However, you could get a 0.50% rate discount if you have a U.S. Bank checking or savings account and sign up for automatic payments.

- Does not charge origination, late payment or prepayment fees

- Direct payment to creditors is available

- Offers relationship banking benefits

- Offers both co-signer and co-borrower options

- Minimum credit score of 680 required

- No live chat support option

- Extended phone hours only (not available 24/7)

- Average 2-day funding timeline

Lender Details

Eligibility

- Minimum credit score: 680

- Co-signers/co-borrowers: Accepted

Funding Speed

You could get your loan within four business days after approval.

BEST FOR CURRENT WELLS FARGO ACCOUNT HOLDERS

PenFed

Minimum Credit Score

Not disclosed

APR range

8.99% to 17.99%

Not disclosed

8.99% to 17.99%

Although PenFed was originally created to serve U.S. military members and veterans, in addition to federal employees and retirees, it has expanded its membership to non-military members. PenFed has several federal partners, including the American Society of Military Comptrollers, Coast Guard Auxiliary Association, Navy League of the United States and United States Army Warrant Officers Association.

PenFed offers fixed-rate, low-interest loans that start $600 to $50,000. If you’re looking for a mix of low interest rates and high loan limits, PenFed may not be the choice for you; look toward LightStream for higher limits.

PenFed personal loans carry rates from 8.99% to 17.99%, based on your application and credit information. Applicants with higher credit scores can typically snag the lowest rates. What’s more, PenFed also boasts no title or deed requirements, no early payoff penalty and no origination or hidden fees. Although PenFed is located on the East Coast, borrowers will have around-the-clock access to their accounts through the PenFed mobile app.

Anyone can apply for a loan through PenFed; however, if you’re approved and choose to move forward with your loan, you’ll need to become a member of the credit union. Becoming a member is easy, and it typically only takes a few minutes. While the membership is free, you’ll need to make a deposit of at least $5 into a new PenFed savings account.

- Interest rate cap lower than many other lenders

- No origination fee

- Must become a member to qualify

- No discount for using autopay

Lender details

Eligibility

- Minimum credit score: Not disclosed

- Co-signers/co-borrowers: Yes

Funding Speed

Next-day funding may be available. The speed of funding may be longer or shorter depending on what time of day you apply for a loan.

Most Popular is calculated from the number of times each affiliate product was selected by Forbes Advisor users over a six month time period.

Tips for Comparing Low-interest Personal Loans

Consider these tips when comparing low-interest personal loans:

- Look for autopay discounts. Not all providers offer interest rate discounts when you set up automatic payments, but most top providers do. When looking at different low-interest personal loans, take into consideration which ones offer an additional rate discount to help you receive the lowest rate possible.

- If possible, prequalify with a provider. Several providers offer the opportunity to prequalify you for a personal loan. This means you can submit details like your income, desired loan use, housing situation and other information to learn about potential loan limits, rates and repayment options. Prequalifying also only requires a soft credit check, which doesn’t hurt your credit score, so you can safely find the best rates.

- Check for additional fees. Some personal loan providers charge no origination fees, late payment fees or prepayment penalties. However, there are some that may charge all or a few of these fees. When comparing low-interest personal loans, be sure to look at the fee structure beyond the potential interest rate you can receive.

- Evaluate the lender’s customer support options. If you’ve found a lender, there’s one more thing to consider before signing the loan agreement. While customer support may not seem like a big deal, it can make a huge difference if you encounter issues with payments or face a financial hardship during your repayment period. Review the lender’s customer service resources and read reviews to make sure it’s a good fit.

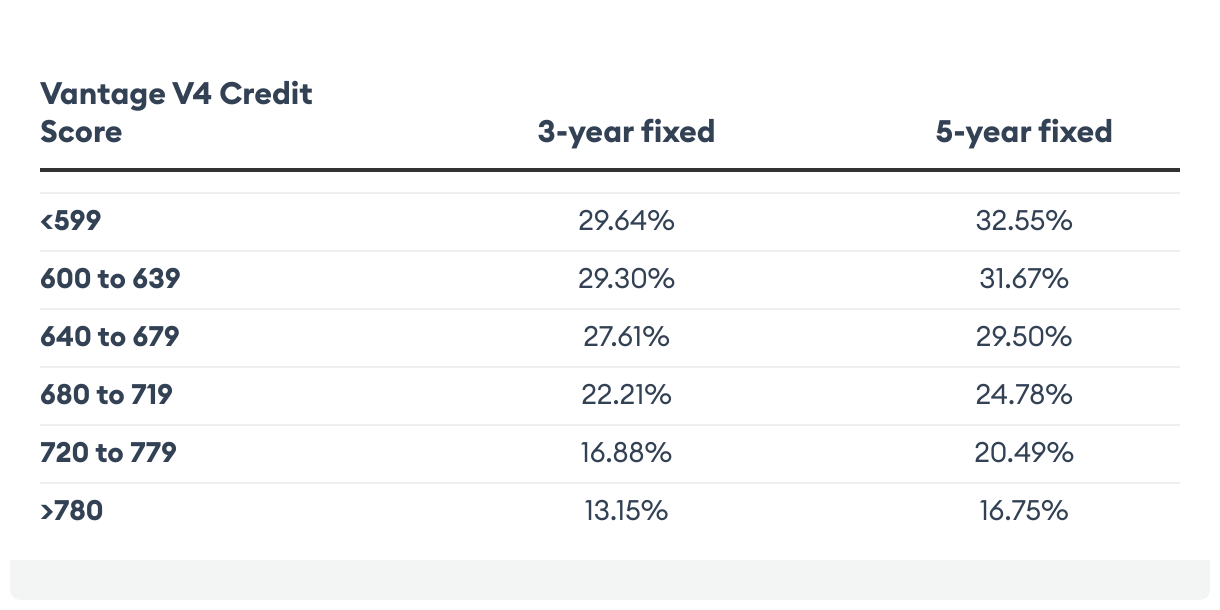

Average Personal Loan Interest Rates

Having good credit saves you money. If you have poor credit, you’ll pay more than twice as much in interest as someone with an excellent credit score.

Factors That Affect Your Personal Loan Rate

Lenders calculate personal loan interest rates based on a number of variables ranging from the borrower’s creditworthiness and income to the size of the loan and repayment term. Factors that can impact personal loan interest rates include:

- Credit score. Borrowers with higher credit scores—ideally at least 720—are more likely to qualify for the lowest interest rates than applicants with low scores.

- Debt-to-income ratio. A borrower’s debt-to-income (DTI) ratio is the percentage of their income that goes toward their monthly debt obligations. The higher a borrower’s DTI, the riskier they are to the lender, and the higher the interest rate the lender will likely offer. Lenders prefer a DTI of 36% or less.

- Employment. Applicants who are employed in a salaried role generally qualify for lower interest rates than those who freelance, have a new small business or are otherwise self-employed. This is because lenders consider traditional employment more stable from an income and repayment standpoint.

- Income. Lenders also evaluate the sufficiency of an applicant’s income. Minimum income requirements are generally low—around $20,000 annually—but the lowest rates are reserved for those with higher incomes.

- Loan amount. The size of a loan can impact interest rates because the larger it is, the more risk to the lender. For that reason, high-principal loans often come with higher interest rates than smaller loans.

- Loan term. The length of a personal loan repayment period also may impact the interest rate. Generally speaking, the longer the loan term, the higher the interest rate. Borrowers also encounter greater costs with long-term loans because they pay interest over a longer period of time.

- Benchmark rates. Underlying benchmark rates like the Secured Overnight Financing Rate (SOFR) and its predecessor, the London Interbank Offered Rate (Libor), dictate the interest rates available to lenders. The SOFR is based on the interest rates paid among large financial institutions for overnight loans—essentially the costs of short-term borrowing.

The Importance of Low-interest Personal Loans

While personal loans are a handy way to access financing, they can be costly. In addition to repaying your loan amount, you’ll also owe interest every month—higher interest rates result in more expensive loans. This means low-interest personal loans can help reduce the total cost of your loan.

For example, let’s compare three interest rates on a 36-month, $10,000 loan to understand how rates impact the cost of a loan, according to the Forbes Advisor personal loan calculator.

| Loan amount | Interest rate | Loan term | Total interest paid | Total amount paid, including interest |

|---|---|---|---|---|

|

$10,000

|

3%

|

36 months

|

$469.24

|

$10,469.24

|

|

$10,000

|

12%

|

36 months

|

$1,957.15

|

$11,957.15

|

|

$10,000

|

21%

|

36 months

|

$3,563.02

|

$13,563.02

|

Pros and Cons of Personal Loans with Low Interest

Low-interest loans aren’t right for everyone, but if you need them, they can really help you out. Here are some advantages and disadvantages to consider as you make a decision.

Pros

- Offers access to more affordable debt

- Fewer interest charges over the life of your loan

- Quick funding within a matter of a few business days

- Can help you build credit if you make all your payments on time

Cons

- Reduces flexibility in your monthly budget

- You could be sued if you default

- Causes a small temporary dip in credit score when you apply

- Diverts money that you could use elsewhere, like building an emergency fund

Where To Get Low-Interest Personal Loans

You can find low-interest personal loans from many different lenders, so shop around before you apply for a loan.

Typically, credit unions and online lenders offer the lowest personal loan interest rates. Getting pre-approval from various lenders can allow you to see which rates you qualify for without impacting your credit score.

You can then compare your offers and submit an application where you are offered the lowest interest rates on a personal loan.

How To Qualify

The best rates on personal loans go to applicants who can demonstrate they’ll be able to easily repay a loan. Here’s how you can boost your odds of getting the lowest possible rate on a loan:

- Build your credit. The lowest-rate personal loans go to applicants with excellent credit scores, often 800 or higher. Building your credit history can take time, but it can pay off with lower interest rates.

- Pay off high-interest debt. Lenders often charge higher rates for applicants with higher debt-to-income ratios, which shows how much of your income goes to debt payments each month. If you pay off some of your debt—especially credit card debt—you can lower this number and increase your odds of getting a lower rate.

- Increase your income. You can also lower your debt-to-income ratio by increasing your income, which shows lenders you can fit debt payments into your budget.

- Use collateral. Collateral, or something of value your lender can repossess if you default on the loan, can help you qualify for a lower rate on your loan if you’re applying for a secured loan.

- Find a creditworthy cosigner. A quick way to become a more attractive borrower is to ask someone with good credit to co-sign your loan. Keep in mind, if you fail to repay the loan, your co-signer will be expected to repay the debt.

- Shop around. Each lender offers different rates. The more lenders you check your rate with, the better your odds of finding the lowest-cost loan.

- Choose a shorter term length. Shorter-term loans come with higher monthly payments, but lower overall loan costs. Shorter-term loans are less risky for the lender, so they often come with lower interest rates.

How to Get a Low-interest Personal Loan

While the process varies by lender, follow these general steps to apply for a personal loan:

1. Check your credit score. Check your credit score for free through your credit card issuer or another website that offers free scores. This will give you an understanding of your creditworthiness and your qualification chances. While you can qualify for a low-interest personal loan with a credit score as low as 650, you won’t receive the lowest possible rates; a score of at least 720 will yield the most favorable terms.

2. If necessary, take steps to improve your credit score. If your score falls below 650 or you want to boost your score to receive the best terms possible, take time to improve your score before applying, such as lowering your credit usage or paying off unpaid debts.

3. Determine how much you need to borrow. Once you check your credit score, calculate how much money you want to borrow. Remember, though, you’ll receive your money as a lump sum, and you’ll have to pay interest on the entire amount—so only borrow what you need.

4. Shop around for the best terms and interest rates. Many lenders will let you prequalify prior to submitting your application, which lets you see the terms you would receive with just a soft credit inquiry. Prequalifying lets you shop around for the best rates without hurting your credit score.

5. Submit a formal application and await a lending decision. After you find a lender that offers you the best terms for your situation, submit your application online or in person. Depending on the lender, this process can take a few hours to a few days.

Related: 5 Personal Loan Requirements To Know Before Applying

Can You Get Low-interest Personal Loans With Bad Credit?

The best low-interest personal loans require a minimum credit score of 650. However, a bad credit score, according to FICO, is between 350 and 579. Applicants with bad credit scores shouldn’t expect to qualify for low-interest personal loans, or even the lowest rates on bad credit loans. The best rates, regardless of the type of loan, are reserved for highly qualified applicants.

If you have bad credit but want to get a low-interest personal loan, take time to improve your credit score before applying. This extra step can lower the cost of your loan and make your repayment easier to handle.

Alternatives to Consider

If you need to borrow money to consolidate debt or make other purchases, a low-interest personal loan is one of the best tools for the job. However, if it doesn’t seem right for your situation, consider other alternatives.

1. 0% APR Credit Card

Some credit cards have special 0% annual percentage rate (APR) introductory offers for up to nearly two years. If you pay off your balance before the introductory period ends, it’s essentially a free loan. However, any unpaid balances once the introductory period closes will be charged with the normal interest rate.

2. Home Equity Loan or Line of Credit

If you’re a homeowner, one option might be a home equity loan or line of credit. If you have substantial equity in your home, these allow you to borrow against that equity at a relatively low interest rate. However, if you default on the loan, you risk losing your home because it serves as the collateral that backs the transaction.

3. Friends and Family

If you’re not able to take out any debt at all and you absolutely need some cash to tide you over, consider turning to your social system for support. Reach out to family and friends and ask to borrow some cash. You can even offer to write and sign a loan agreement to show you’re serious about paying it back in a timely manner.

4. Cash-Out Refinance

A cash-out refinance involves replacing your existing mortgage with a new, larger mortgage. You then pocket the difference between the two mortgages, and you can use that money for any expense.

This can be a good option if you can qualify for lower interest rates on the cash-out refinance and have sufficient equity in your home. Keep in mind, even if interest rates are lower, you’ll pay closing costs of 2% to 6% of the total amount.

How We Picked the Best Low-Interest Personal Loans

How We Evaluate the Best Low-Interest Personal Loans

-

58

Lenders researched

We chose which lenders to review based on loan volume and availability

-

5

Methodology factors considered

Includes cost, loan details, accessibility, customer experience and application proc

-

15

Metrics examined

Most weight given to loan costs and accessibility

| Product Name | Consumer Sentiment Index | Interest Rates and Fees | Customer Service | Loan Terms and Flexibility | Ease of Approval and Process | Overall Satisfaction |

|---|---|---|---|---|---|---|

|

LightStream

|

|

3/10

|

2/10

|

4/10

|

3/10

|

3/10

|

|

SoFi

|

|

3/10

|

3/10

|

3/10

|

4/10

|

3/10

|

|

Wells Fargo

|

|

2/10

|

2/10

|

3/10

|

2/10

|

3/10

|

|

U.S. Bank

|

|

3/10

|

3/10

|

1/10

|

4/10

|

3/10

|

|

PenFed

|

|

3/10

|

3/10

|

3/10

|

4/10

|

3/10

|

Former Staff Editor

Staff Editor

Jordan Tarver

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor’s degree in business finance, his experience as a top performer in the mortgage industry and his entrepreneurial success to simplify complex financial topics.

Mike Cetera

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The Points Guy and Fit Small Business. He also has offered his expertise in numerous TV, radio and print interviews.

Jordan Tarver

Jordan Tarver has spent seven years covering mortgage, personal loan and business loan content for leading financial publications such as Forbes Advisor. He blends knowledge from his bachelor’s degree in business finance, his experience as a top performer in the mortgage industry and his entrepreneurial success to simplify complex financial topics.

Frequently Asked Questions (FAQs)

What is a good interest rate on a personal loan?

Personal loan interest rates vary depending on your lender and credit score. If you have a high credit score, you could see interest rates as low as 2.49%, depending on where you get your loan. However, if you have poor credit scores, you may only qualify for loans that charge interest rates of 20% or more. Before you apply, improve your credit as much as possible to increase your odds of landing the best interest rate possible.

Which bank has the lowest interest rate on a personal loan?

If you have a strong credit score, you can receive the lowest interest rate through LightStream. LightStream has rates as low as 2.49% if you enroll in autopay. Other lenders, like SoFi, PenFed, Wells Fargo, Marcus and U.S. Bank, offer rates as low as 5.99%. Although not as low as LightStream, rates that low still beat out other methods of financing, including credit cards.

How can I get a low-interest personal loan?

Before applying for a low-interest personal loan, check your credit score. If your score is low, look to improve it first. Some lenders let you prequalify with a soft credit check, which lets you see what type of loan terms you could receive with your current score. Once you find a loan that offers favorable terms for your financing needs, apply with the provider. If you qualify, be sure to set up autopay to earn potential discounts and avoid any late payment fees.

How can you get a low-interest personal loan with great credit but no job?

Unfortunately, loan qualification is not solely based on your credit. Most lenders require you to provide proof of your income with past tax returns, bank statements and pay stubs. Your income demonstrates your ability to repay your loan and helps determine the amount of money you qualify to borrow.

If you don’t have a job but have other income sources, you might be able to use those to qualify for the loan. Lenders might accept income from the following sources:

• Interest and dividends

• Social Security

• Long-term disability

• Alimony or child support

• Trust fund

• Rental property

• Retirement or pension

While some lenders will let you take out a loan with no income or allow you to use nonemployment income to qualify, it’s still not a good idea to take one out if you can’t afford to repay it.

How do you consolidate credit card debt with a low-interest personal loan?

If you have debt on multiple credit cards, you can apply for a debt consolidation loan to help lower your interest rate, streamline payments and improve loan terms. Many debt consolidation lenders pay off your other debts directly—or you’ll take the cash and pay off your outstanding balances. After your pre-existing debts are repaid with the new loan funds, you’ll make a single payment on the new loan each month.