9

6 Best Banks and Credit Unions for Military in 2023

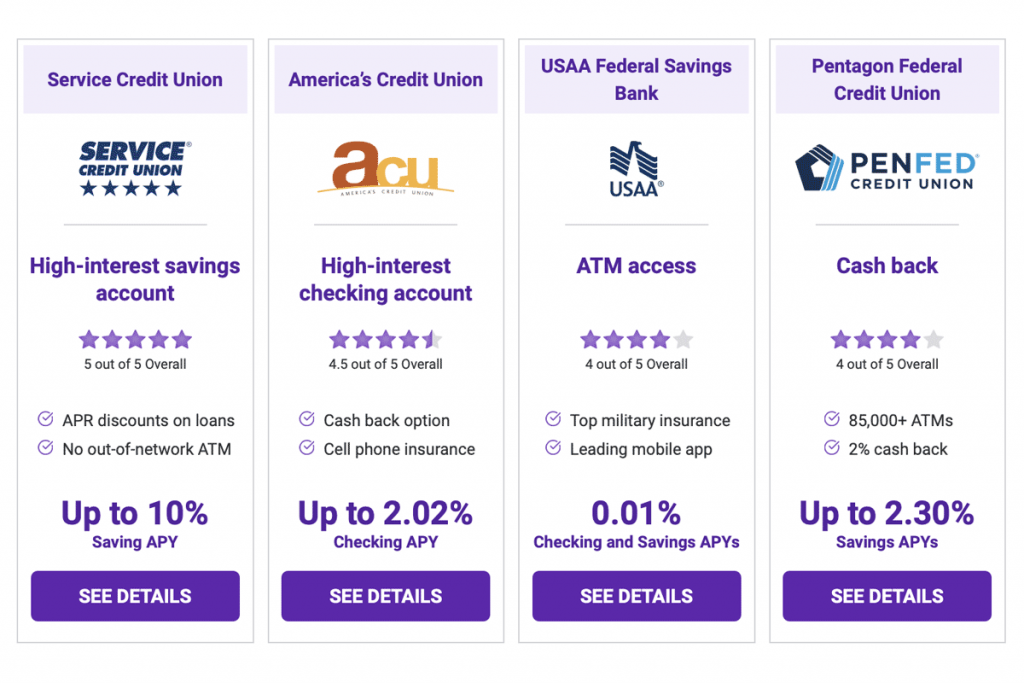

Service Credit Union

High-interest savings account

Up to 10%

Saving APY

America’s Credit Union

High-interest checking account

Up to 2.02%

Checking APY

USAA Federal Savings Bank

ATM access

0.01%

Checking and Savings APYs

Pentagon Federal Credit Union

Cash back

Up to 2.30%

Savings APYs

6 Best Military Banks and Credit Unions

Members of our military, whether active duty or veterans, have access to unique bank accounts from both banks and credit unions.

Such accounts are uniquely designed to suit the specific needs of active duty members (easy online bill pay, international branches on bases and 24/7 stateside assistance, for example) but also honor both active members and veterans for their service via a higher annual percentage yield (APY), better insurance rates, lower annual percentage rates (APRs, or interest rates) on loans and other great benefits.

If you or your spouse currently serves or has previously served as a member of the US military and you are looking for a bank account that meets your needs, consider one of these six military banks and credit unions:

Below, we’ve explored each military bank in detail, focusing on their checking and savings accounts primarily, though we’ve also made note of other features, including credit cards, loans, insurance and investment accounts.

In determining our list of the best military banks and credit unions, we considered:

While these six are the elite (think of them as the best of the best banks for military personnel), some national financial institutions also offer special accounts for active duty military members, veterans and their families. These bank accounts include:

We did not include the national financial institutions offering specific military accounts in our consideration, though they are certainly worth exploring for your banking needs if the actual military banks don’t seem to be the right fit.

With up to 10% APY, Service Credit Union easily boasts the highest APY of any bank on our list thanks to the Deployed Warrior Savings. If you are an active duty member of the US military serving in a combat zone, there should be no question about it. This should be where you save all your money.

But Service CU is ideal for military members for more than just offering amazing APYs on its savings account. It also boasts a free Everyday Checking account (and a Dividend account) with unique tiers that grant up to $30 a month in ATM surcharge reimbursement and up to a 0.75% APR discount on loans. These checking accounts also include online and mobile banking, early direct deposit and ID theft protection.

Service CU is great for military members deployed in Europe thanks to its multitude of branches abroad. Back home, Service CU is mostly focused in the Northeast with a location in North Dakota, but with the ease of online banking, you can hold a Service CU account from anywhere.

In addition to the savings and checking accounts, Service CU offers business banking, vehicle loans, home loans, credit cards, personal loans, student loans and military loans. You can also rely on Service CU for investment services, insurance certificates, trusts and money market accounts.

Eligibility: Active duty military, veterans and their family members; Department of Defense employees; members of select employer groups; and other select groups

Service CU may have the best of all the savings accounts on our list of the best military banks and credit unions, but then America’s Credit Union has the best checking account. In fact, America’s CU offers several great options for checking accounts.

The headliner account is Affinity Basic, which pays 2.02% APY on up to $1,000 — then 0.10% on additional funds up to $15,000 and 0.25% on funds exceeding $15,000 (but you probably shouldn’t keep that much in a checking account). This high-yield checking account has no monthly maintenance fees or minimum balance requirements and offers online and mobile banking.

The Affinity Premier account requires a $25,000 opening balance, pays a 0.75% APY on funds up to $34,999 and pays market rate on dividends.

The only account with a monthly service fee is the Affinity Plus ($7 a month), but this account gets you 10 cents cash back for every swipe of your debit card, as long as you spend at least $5. (At most, that’s 2% cash back.) This account also pays 0.75% APY on any balance up to $25,000, which makes it better than a lot of standard savings accounts. The account even includes identity theft coverage, cell phone insurance and a $10 monthly ATM fee reimbursement.

America’s Credit Union’s savings account is nothing to write home about: a meager 0.01% APY on balances below $2,500, and even then, just 0.10% APY on $2,500 and higher. The Guaranteed Money Market Ultra account has more appeal, with 1.76% APY on balances above $2,500.

America’s CU does offer a variety of loans: home loans, personal loans, student loans and auto loans, as well as rewards credit cards. You can also use America’s CU for business banking and investment services.

Eligibility: Members of the Armed Forces, civilian personnel and their relatives; members of the Association of the United States Army; members of the Pacific Northwest Consumer Council (or PNW residents willing to donate to the council — ACU will cover the cost!). Family members of current members may also join.

Upon first glance, USAA might not seem like the best financial institution for members of the military. The checking account’s APY is almost nonexistent (and only kicks in if you have more than $1,000 in the account), and the APY for the basic savings account is just as low.

You can earn more interest with the USAA Performance First, but the tiered account doesn’t start paying out competitive interest (0.50%) until you have $50,000 in the account and tops out at 1.04% — but you need at least $250,000 in savings.

So why is USAA so popular among members of the military and one of the best military banks and credit unions overall?

For starters, USAA is a household name for military members because of their impressive insurance offerings and super low rates. But in addition to insurance, you can use USAA for retirement accounts, investment accounts, certificates of deposit, credit cards, youth banking and all forms of loans, including home and auto; personal; and motorcycle, RV and boat.

Access to ATMs is nothing to sneeze at with more than 100,000 nationwide (and a rebate of up to $10/month for out-of-network ATM surcharges). Physical branches are limited to just Colorado Springs, Colorado; Annapolis, Maryland; and San Antonio, Texas (two New York branches are temporarily closed).

That said, USAA’s mobile and online banking make it so that your location does not matter. The bank’s app has a 4.8 star rating on the App Store (1.6 million reviews) and a 4.1 star rating on Google Play (nearly 200,000 reviews).

Eligibility: Active Duty, National Guard, Reserves, Veterans who served honorably, Cadets and Midshipmen, plus military spouses and children of USAA members.

You can choose from multiple savings accounts at PenFed CU, including the Regular Savings (0.05% APY and easy ATM access with an ATM card) or Premium Online (2.30% APY, no monthly maintenance fees and free online transfers). You can also open a Money Market Savings account that pays a 0.15% APY on balances over $100,000, but that money would be better invested in a high-yield savings account or, better yet, in a diversified brokerage account.

You can choose from two checking accounts. The PendFed free Checking account has no monthly fees and no minimum balance requirements. You’ll get more perks with Access America Checking. There’s a $10 monthly fee, but you can easily have it waived by either earning a direct deposit totaling $500 or more each month OR just keeping an average daily balance of $500. This is a good idea for checking accounts anyway—to avoid overdraft fees.

Access America Checking earns 0.15% APY on balances less than $20,000, but when you hit that $20K mark, you’ll start earning 0.35% APY.

Some hallmarks of this account, aside from the super convenient ATM access, include a highly rated mobile app and early direct deposit. You can also open a Money Market Certificate, with terms ranging from six months to seven years; right now, it’s paying 4.70% APY on the 18-month term. You can invest as little as $1,000.

In addition to the savings, checking and money market accounts and the certificate, you can utilize PenFed for credit cards, home and auto loans, student loans, personal loans and retirement accounts.

Eligibility: This is the easiest bank or credit union to join on our list. Anyone can apply.

Navy Federal Credit Union offers the most checking account options of any financial institution on our list. This includes the Free Active Duty Checking (with $20 of monthly ATM fee reimbursements); Free Easy Checking (with Checking Protection Options to avoid the $20 overdraft fee); Free Campus Checking (ideal for students of deployed military members); Free EveryDay Checking (nominal APY but no monthly fees); and the Flagship Checking, which boasts up to 0.45% APY and a 0.45% dividend rate.

There is a $10 monthly fee for the Flagship account, but you can get that waived by maintaining an average daily balance of $1,500 a month.

This financial institution is a favorite of deployed military members who are constantly globe-trotting. The 24/7 customer service means you don’t need to worry about time zones when you call in for help, and the mobile banking (with mobile check deposit and online bill pay) is very convenient.

Beyond checking and savings accounts, Navy Federal CU offers loans for motorcycles, boats and leisure vehicles; student loans, home and auto loans; credit cards; and money market and retirement accounts.

Eligibility: Members of the Armed Forces, employees of the Department of Defense, veterans and the family members of all qualifying members.

Security Service Federal Credit Union offers a Basic Savings Account, but the APY is so low (0.05%) that it’s not worth much consideration. (Children may benefit from the Youth Savings Account with the same APY.)

There’s also a basic free checking account (if you opt into eStatements), but you’d be better served by another free checking account elsewhere.

But the paid Power Protected Checking account is worth a second glance. This unique account comes with a handful of extra features for a $6 monthly fee:

The APY for this account varies widely depending on how much money you keep stored in the account. Balances below $10,000 earn just 0.05%, but if you have $250,000 or more in the checking account (yeah, right), you’ll earn up to 0.79% APY and 1.00% in dividends.

Another plus: There is no minimum balance requirement for this account.

While the accounts and branches are limited to Texas, Colorado and Utah, no worries if you are deployed elsewhere. With shared branching and online banking, you won’t have any problems.

Security Service Federal also offers credit cards, certificates and money market accounts, investment services, IRAs, insurance, and plenty of loans: auto and other vehicles, student and home.

Eligibility: Limited to three states (Texas, Colorado and Utah) and members of select military branches and Department of Defense employees.

Having trouble determining the right financial institution for your needs? We have found that service members should look for these hallmarks of the best military banks and credit unions:

Here are some of the most frequently asked questions from service members when reviewing military banks and credit unions.

Five out of six of the financial institutions on our list are military credit unions. While we can’t say one is the absolute best, this does tell us that credit unions seem to be the better option for service members. That said, USAA is a respectable bank option for full-suite needs while Pentagon Federal Credit Union offers great APY on checking and savings, plus a cash back debit card.

Financial institutions frequently change the bonuses they offer, including military discounts. However, military members should prioritize a bank that has the features listed above. The six military financial institutions on our list, plus the four additional accounts from national banks, are a great place to start.

While most of the accounts on our list have no monthly service fees, most that do carry fees can be waived by meeting simple criteria. In addition, several banks now waive credit card fees for service members. We did not focus on credit cards in our analysis above, but these national credit card companies are noteworthy for waiving annual credit card fees for US military members and their spouses:

Timothy Moore covers bank accounts for The Penny Hoarder from his home base in Cincinnati. He has worked in editing and graphic design for a marketing agency, a global research firm and a major print publication. He covers a variety of other topics, including insurance, taxes, retirement and budgeting and has worked in the field since 2012.

Ready to stop worrying about money?

Get the Penny Hoarder Daily

Some of the links in this post are from our sponsors. We strive to provide accurate, reliable information.

Compensation may influence how and where products appear on our site (including their order), and we do not include all companies or offers.